Am I going to be okay?

Safe-to-spend, a 12-month runway of their real projected balance, and a debt-free date — the whole picture on one screen.

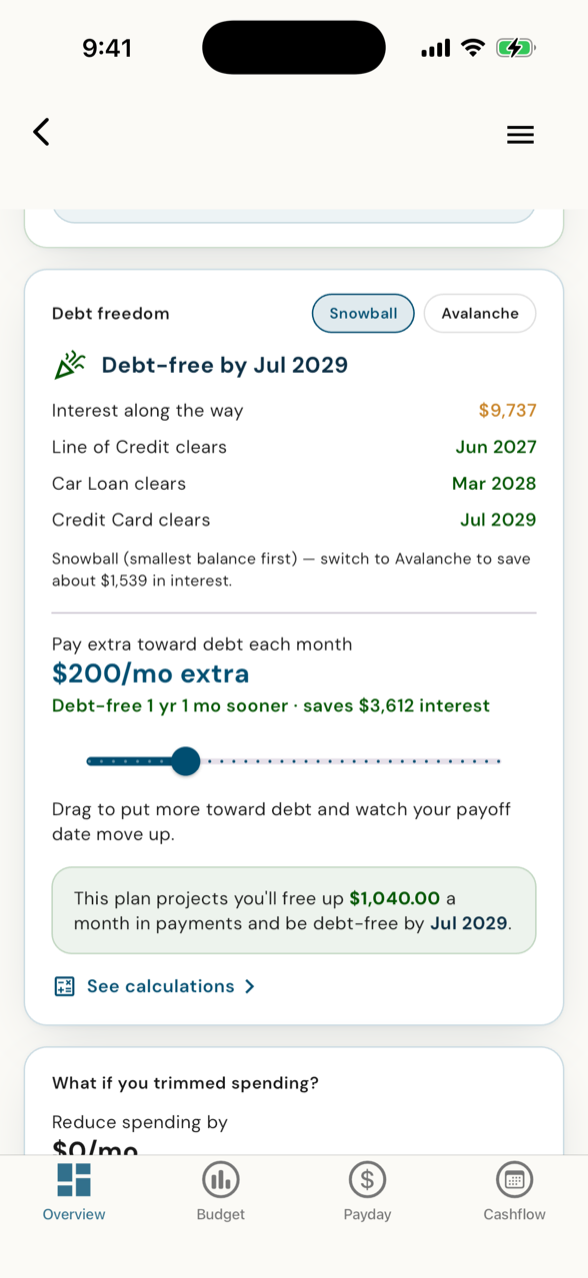

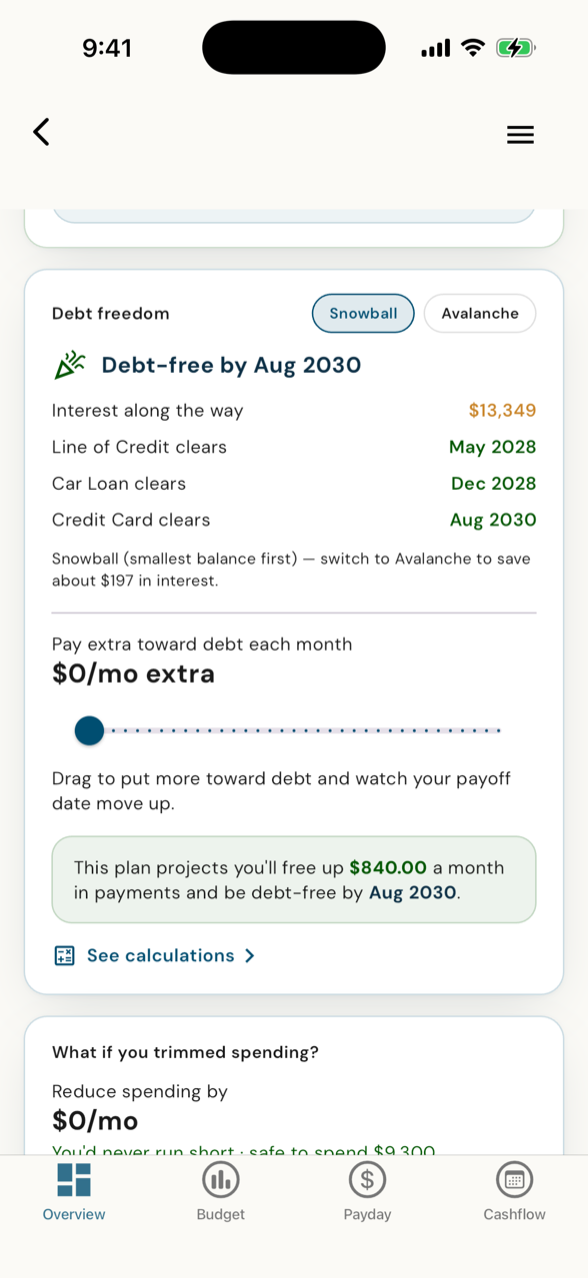

A debt-free date they move with their thumb

Snowball or Avalanche, plus a slider that pulls the payoff date closer the more they put toward debt.

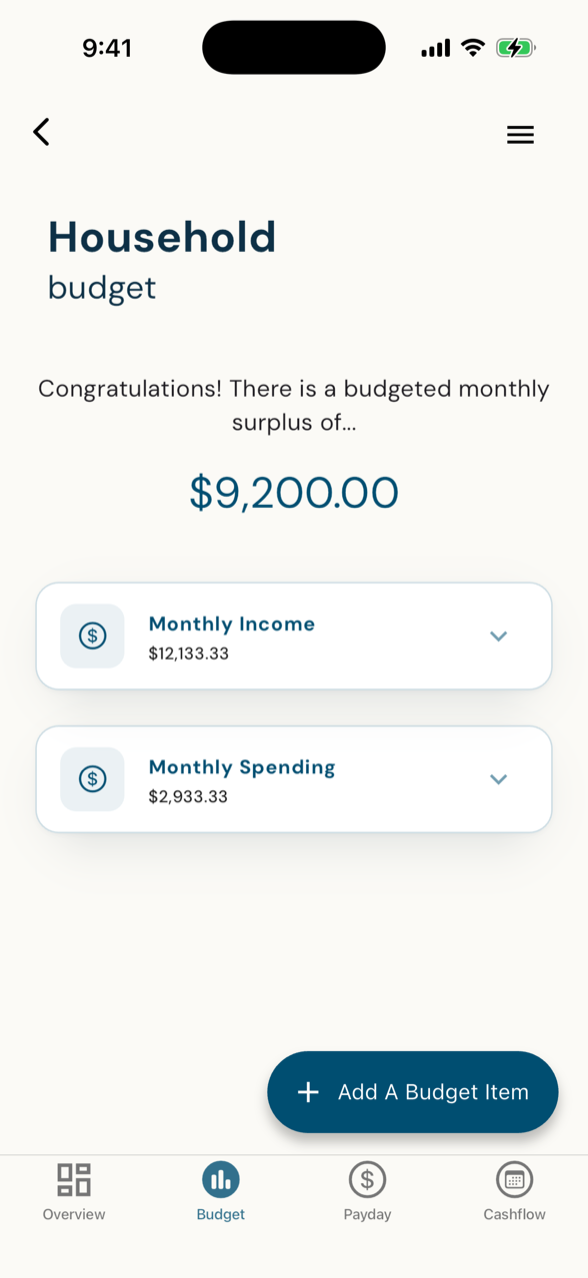

Where the money actually goes

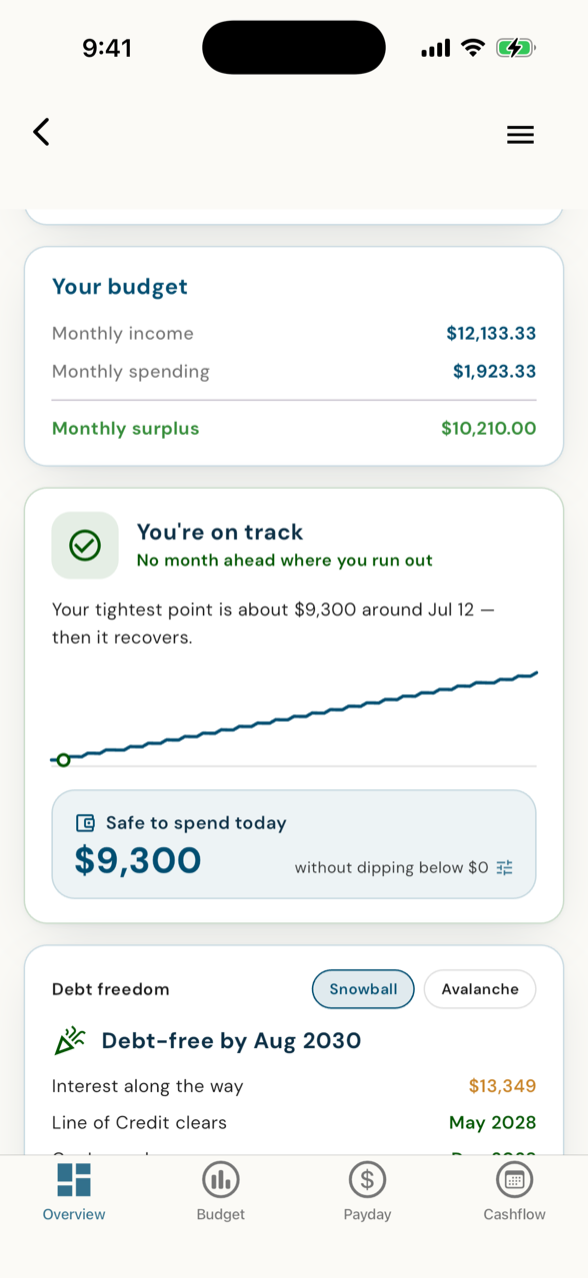

Income and spending by category, with the monthly surplus or shortfall right at the top.

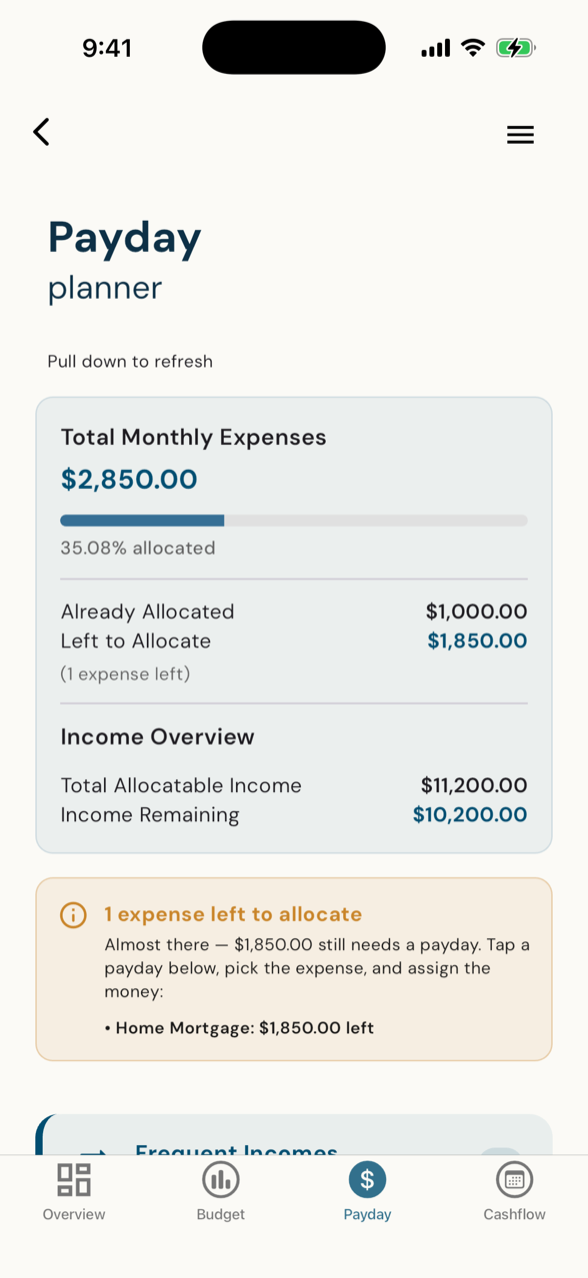

Every dollar has a job by payday

Assign each paycheque the moment it lands. A progress bar shows what's allocated and what's left.

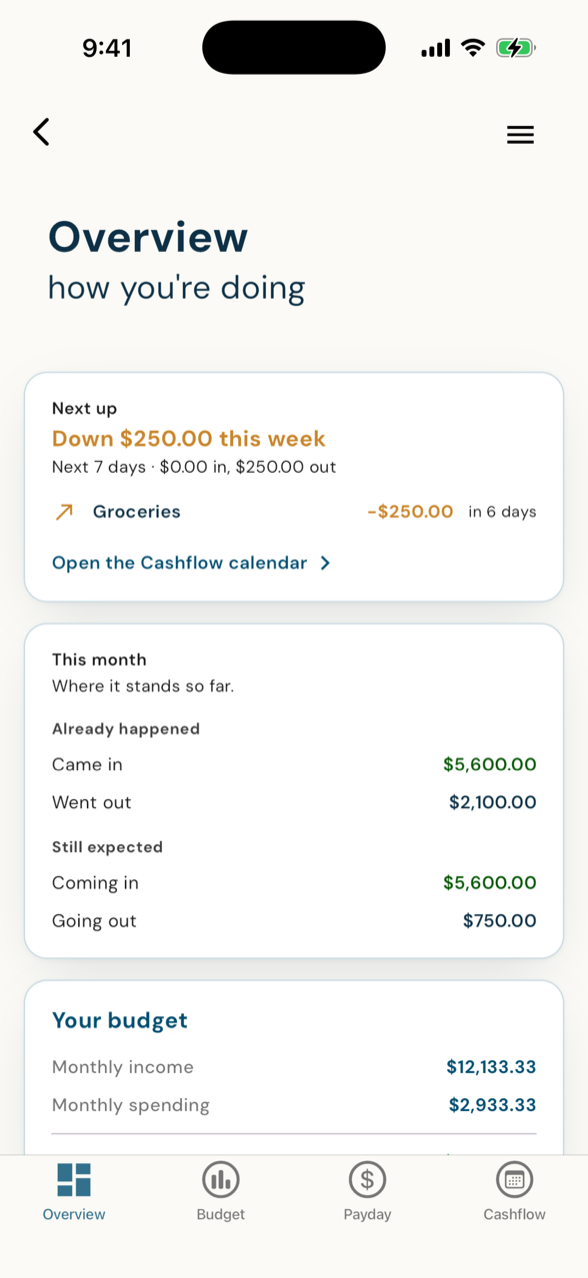

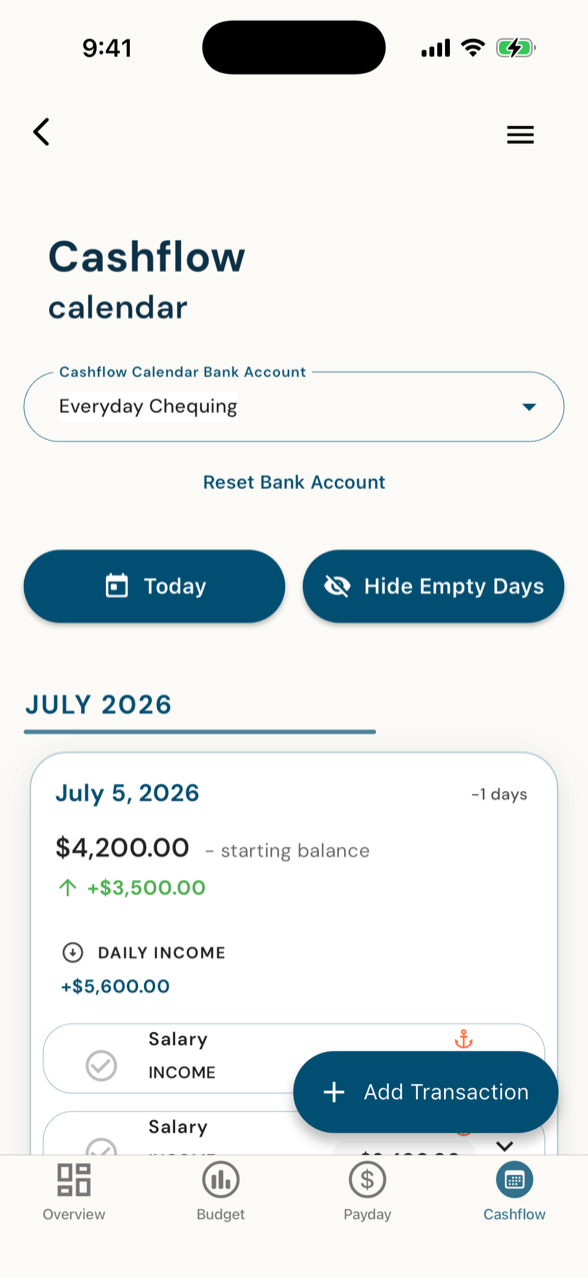

See the squeeze before it happens

Income and bills on one day-by-day calendar, so the tight week in March is obvious in January.

See it coming. Then move it.

Every client carries two quiet questions: when do I get tight, and when am I free? These two screens answer both — a date, a dollar figure, and a dial they turn themselves. Not a snapshot of where the money sits, but a live look at where it's headed. And because they're the ones moving it, the numbers your plan runs on stay current on their own.

See the tight week before it arrives.

Runway plots the real projected balance of a client's bank account a full year out — so the tightest week ahead is circled before it lands, while there's still time to do something about it. Your client isn't reading a static budget. They're watching real projected balances move.

- Real projected balances, day by day. Built from their scheduled income and bills — not a static budget that never blinks.

- A cushion line they set. And a "safe to spend today" number that always respects it.

- Plain-English foresight. "Your tightest point is about $9,300 — then it recovers." The exact week, a year ahead.

- Every visit keeps your plan current. The numbers your plan runs on refresh themselves whenever your client checks in — always today, not last quarter.

Watch the debt-free date move.

Drag one slider and the finish line slides with it — an earlier month, less interest, right there on the card. Snowball for quick wins, Avalanche for the least interest — toggle between them and the math recomputes on the spot. Debt Freedom turns "someday" into a date you can pull closer with your thumb.

- Snowball or Avalanche. Quick wins, or the least interest — toggle and compare the payoff in a tap.

- Slide a little extra toward debt. For example, add $200 a month and the debt-free date jumps 13 months closer.

- The money comes back, dated. The card names the monthly cashflow that frees up the day the last debt clears — real dollars back in the budget.

- Open the month-by-month schedule. As each debt clears, its payment rolls onto the next — so every payoff after it speeds up.

A finish line the client can move themselves — and every time they do, the numbers your plan runs on stay current.

That's the quiet trick underneath all five: your client is the one moving these numbers, so the plan you built refreshes itself the instant they touch it. Not a nicer portal — a client app that also does your data entry for you.

Most software costs you money. This one can pay you back.

It's the only budgeting suite that lives inside the plan — and it's yours to price. Your clients use the app free; the suite — Budget, Debt Freedom, At-a-glance, Payday Planner and Cashflow Calendar — you set client by client: comp everyone, put a fair price on it, or a different number for every client at your table. It's your asset, and you decide what it's worth, one client at a time.

The standalone budgeting apps your clients might grab on their own tend to cost a few dollars a month, every month — yours, in this example, is $29 for the whole year. But price was never the real gap: not one of those apps feeds into the financial plan your client is building with you — they're islands. Yours is the only budgeting suite that lives inside the actual plan, so every dollar your client logs keeps it current the instant they enter it. That's not a cheaper app — it's the only one that's connected.

That's reason one. Reason two is compliance that keeps itself — on every file, and on every life sale.

Two reasons. One app.

Give your clients an app they'll actually open — and let compliance keep itself, on every file and on every life sale. Spin up your shared workspace, invite a client, and watch one live file keep your plan current and your records audit-ready. Your first 5 clients are on us — no credit card.