These three forms are what Client-Level Compliance already maintains on every file — and a life sale can't start until they're signed.

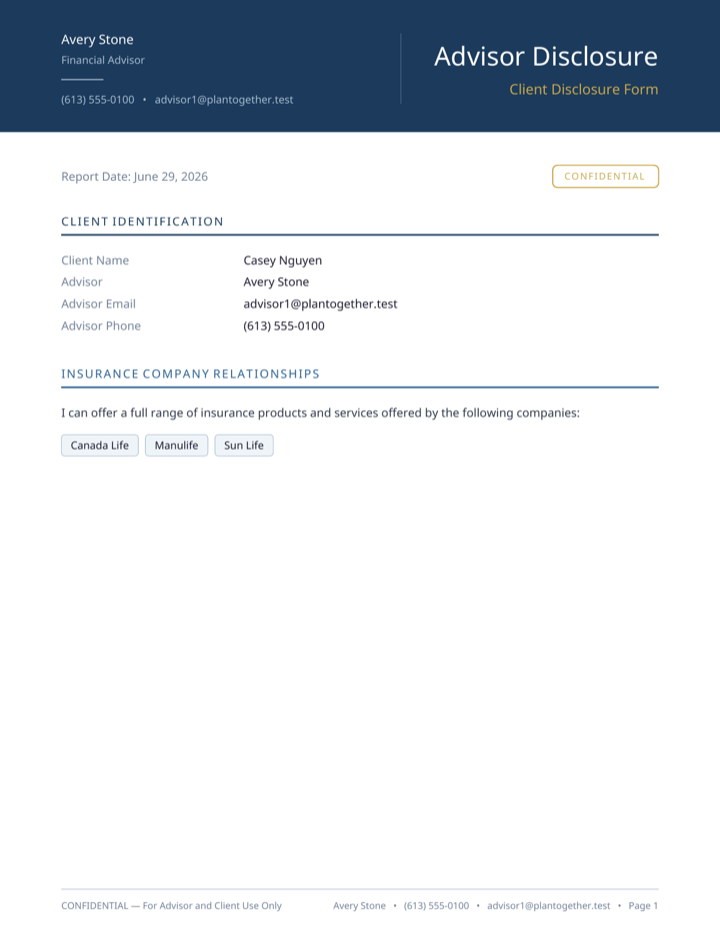

Who you are, what you charge

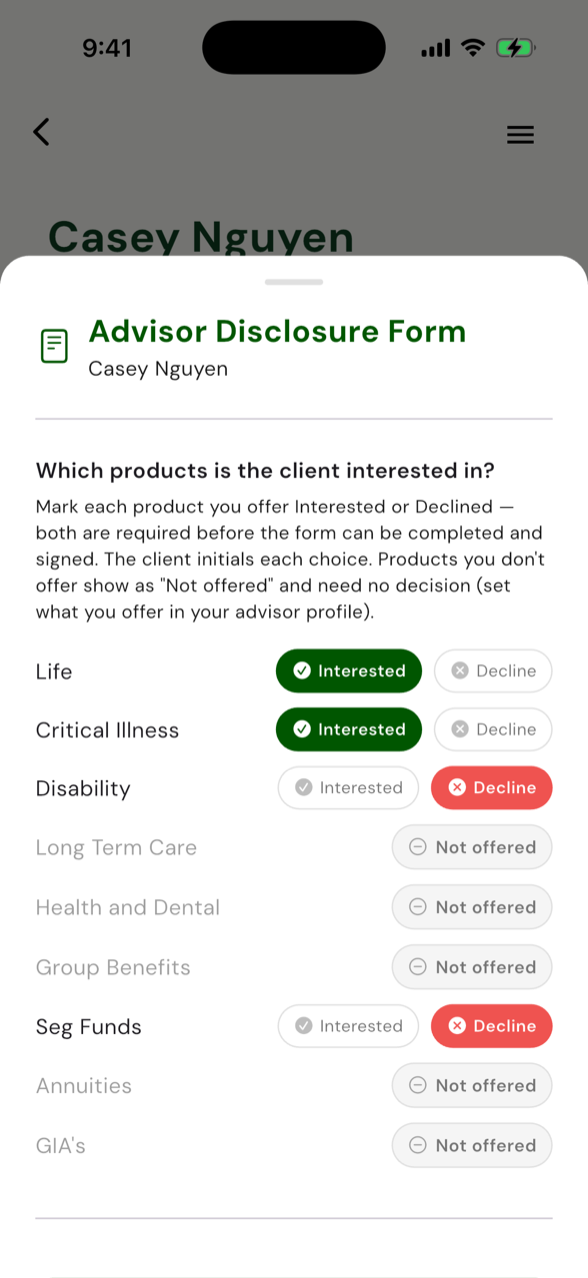

Your licence, carriers and compensation — plus the products you offer, with the ones you don't marked "Not offered."

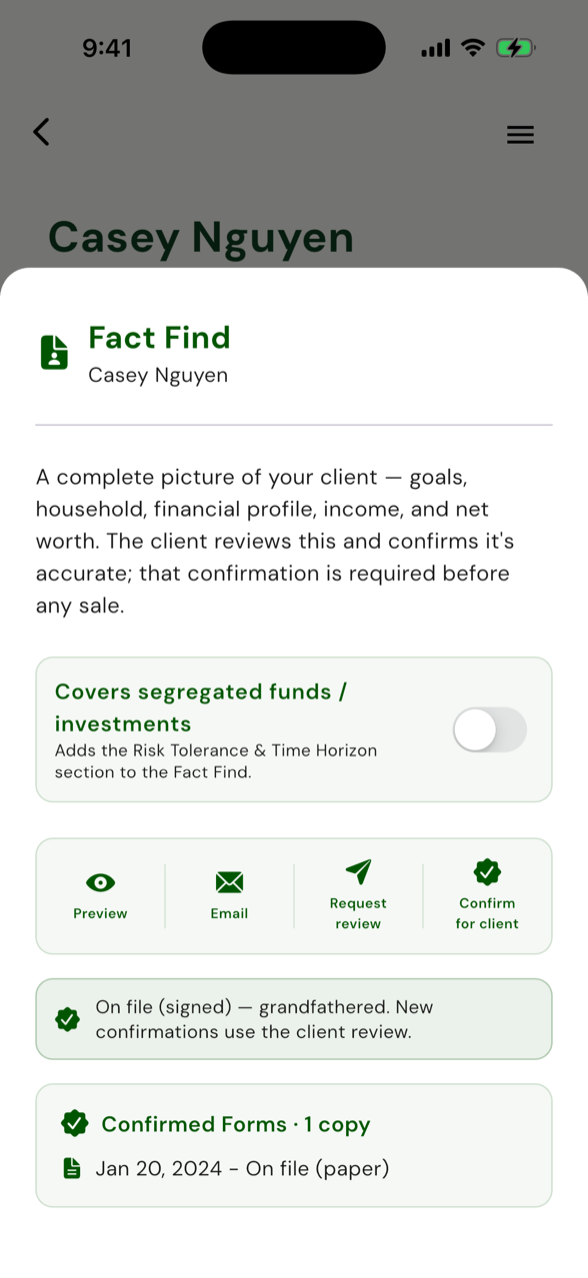

The full client picture

Goals, household, income, debts and net worth — generated from the data on file and confirmed before any sale.

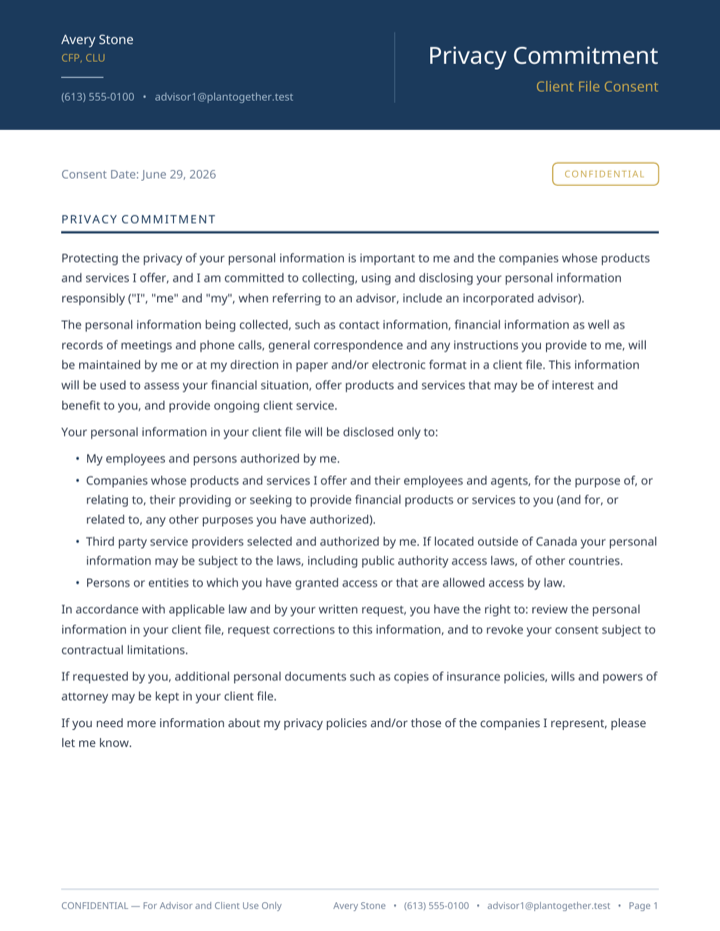

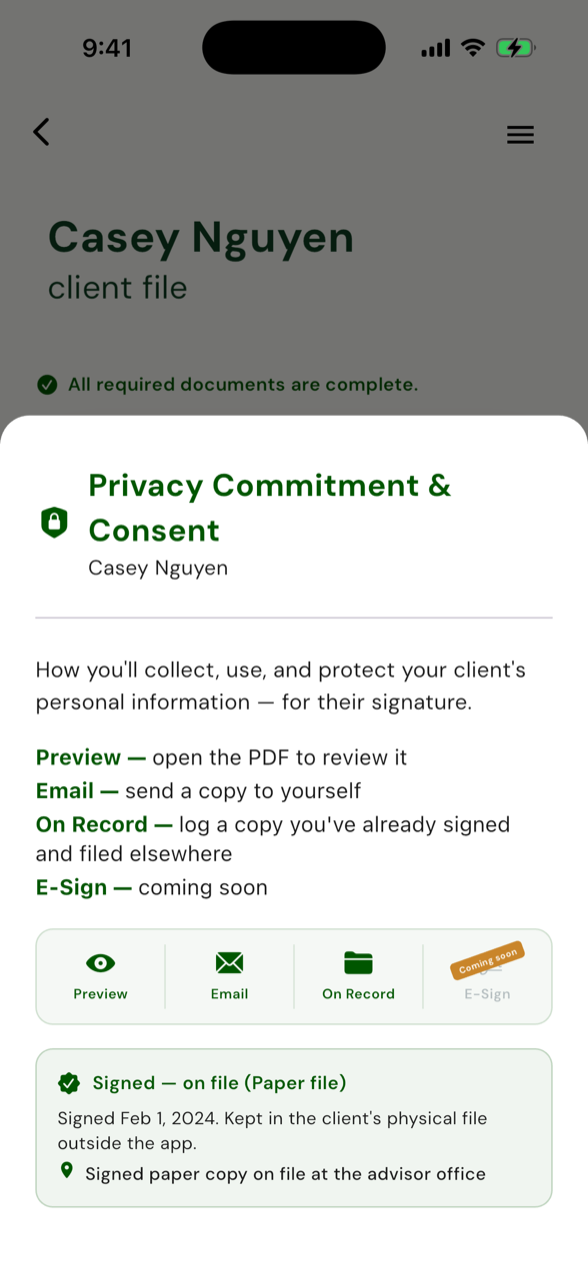

Their data, handled right

How you collect, use and protect their information — preview, get it signed, record the signed copy on file.

The app won't let you do it wrong.

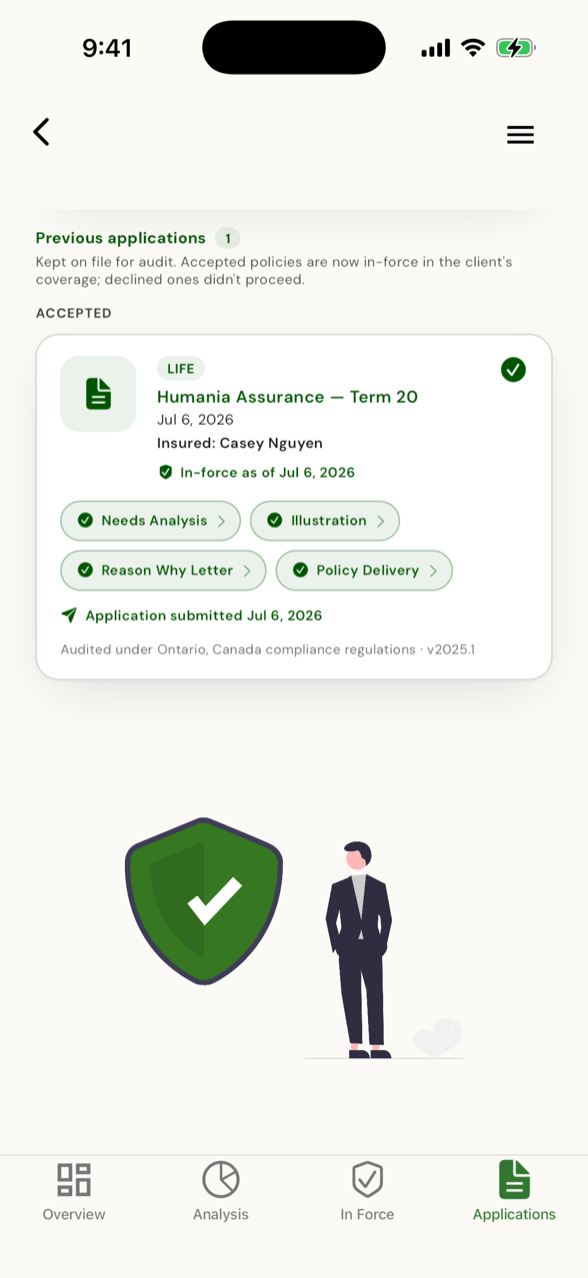

A life sale can't start until the client-level foundation forms are signed. From there, a compliant life sale is four documents in a fixed order, with numbers that have to reconcile and dates that have to line up. Stop hand-assembling that across Word docs and PDFs and praying it adds up — run your next sale through PlanTogether and the right document shows up at the right step, in the right order. The file that comes out the other end is the one an auditor actually wants to see.

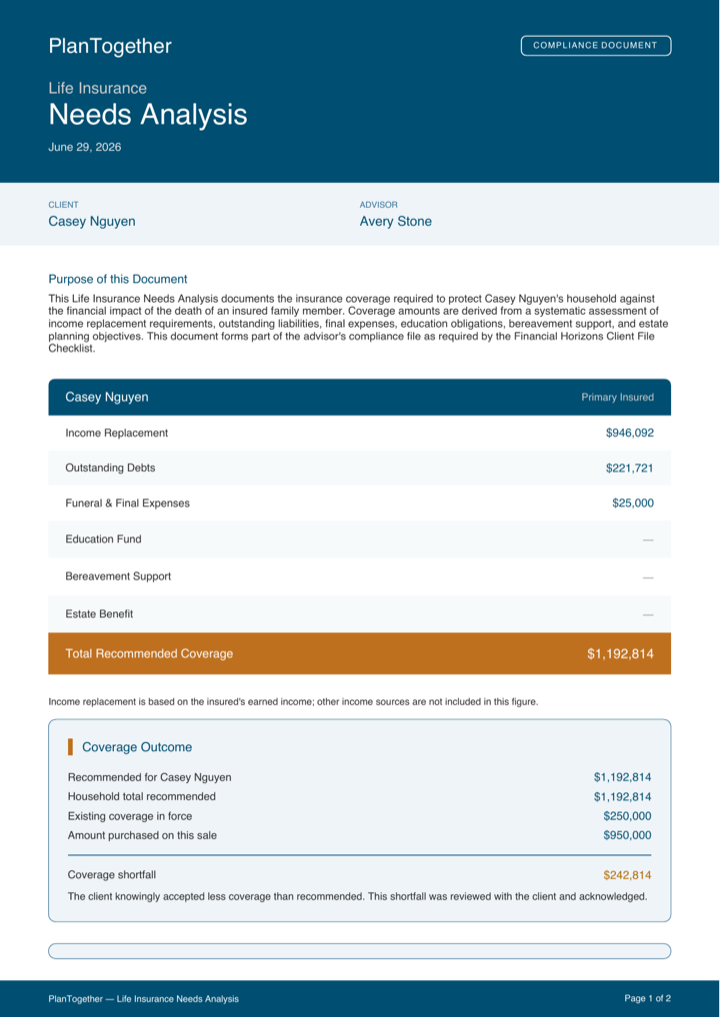

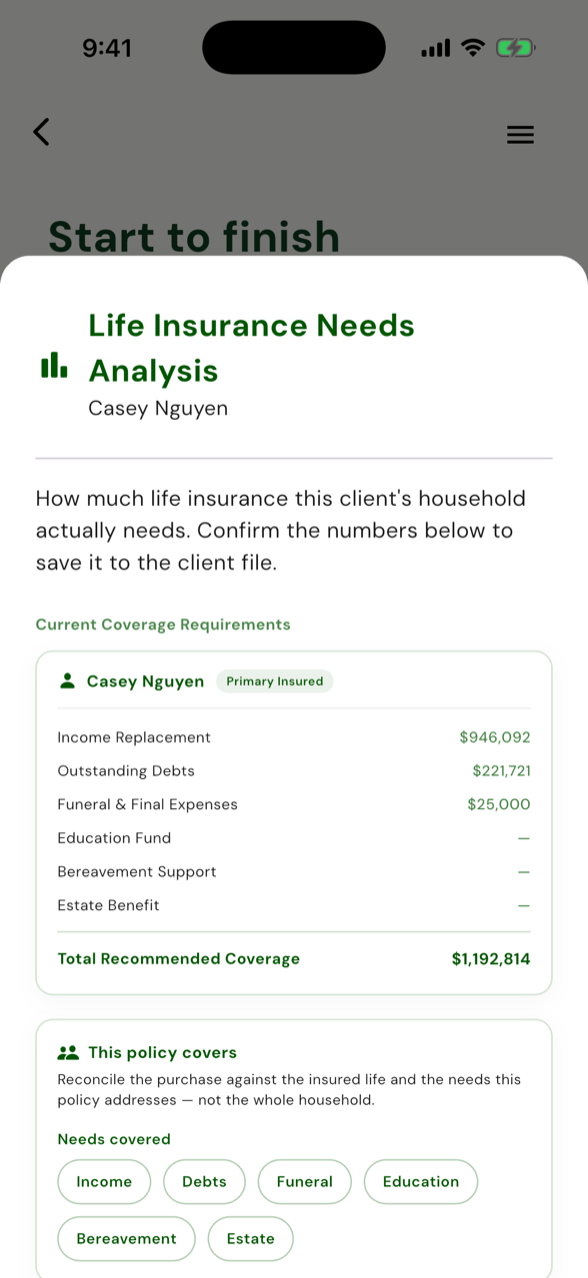

A needs analysis whose numbers reconcile.

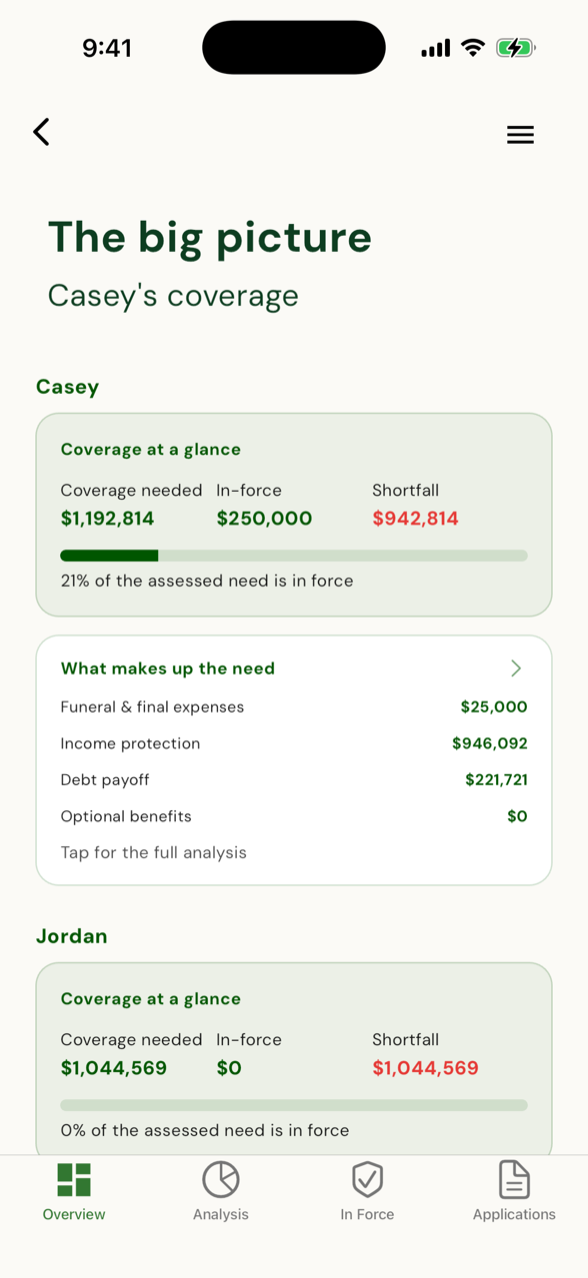

Need, in-force, shortfall — at a glance

Total assessed need, what's already in force, and the gap between them on one screen with a progress bar. The number a client actually understands — and the first thing an auditor opens.

Numbers that actually sum

Final expense, income replacement, mortgage, debts, riders — the breakdown that reconciles to the total. Auditors' number-one finding is needs-analysis math that doesn't add up to the coverage bought. This one reconciles by design.

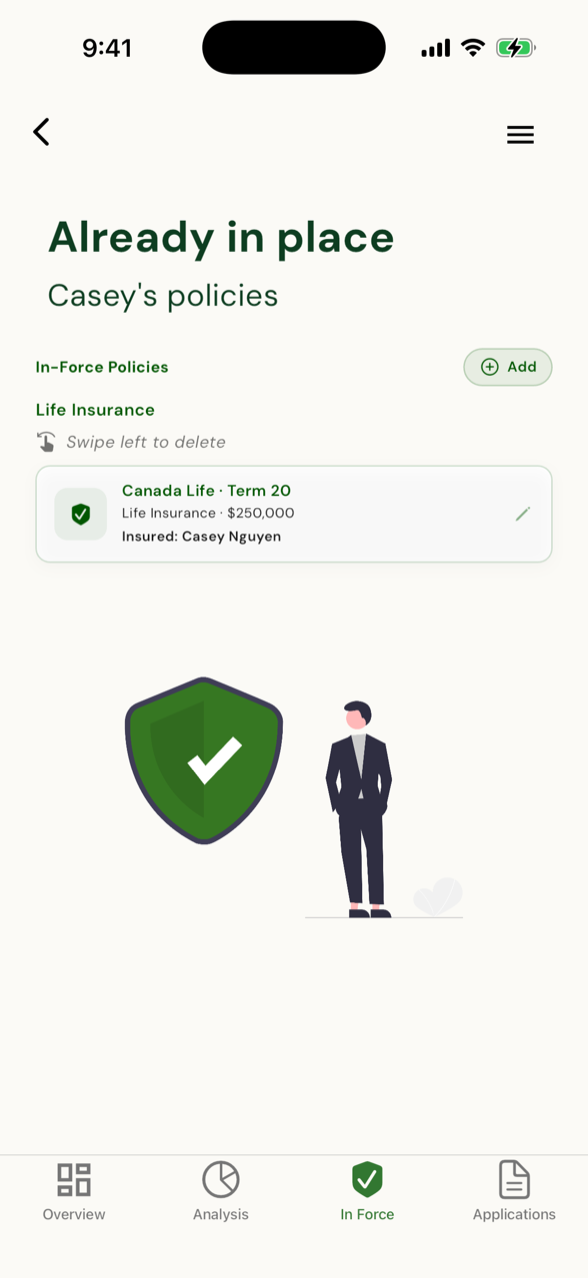

Every existing policy, counted

The client's current policies, pulled into the math instead of guessed at — so the shortfall you're recommending against is the real one, not an estimate.

Each one generated for you — never typed twice.

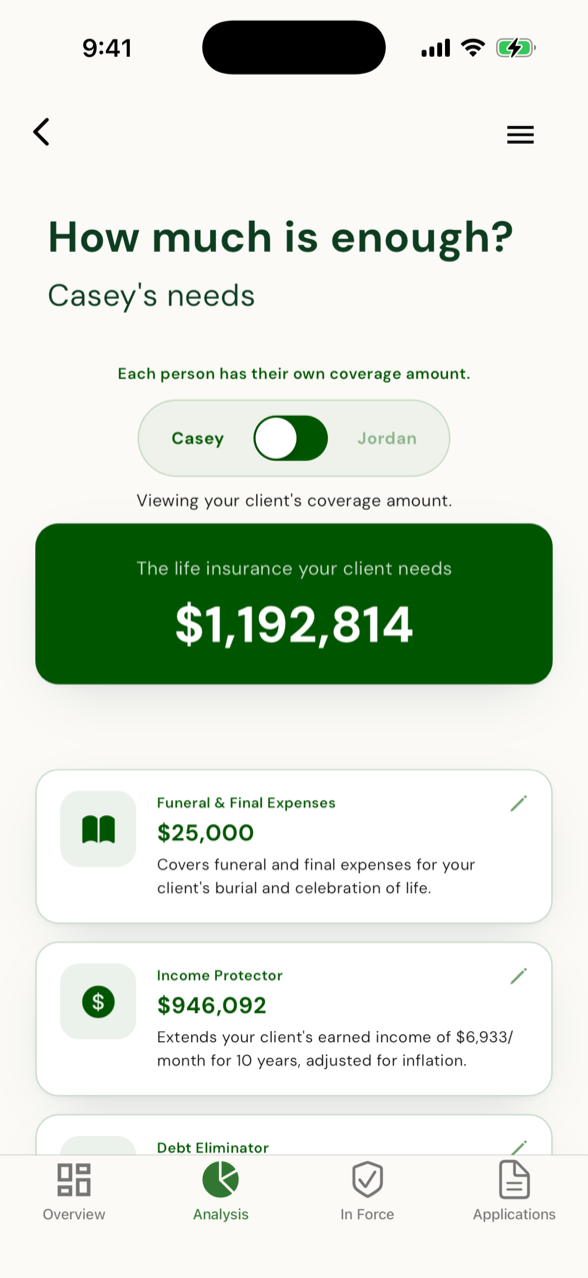

The math that has to reconcile

Quantifies the need per insured life, records what's already in force and what they actually bought — and if they buy less than you recommend, it makes you acknowledge the shortfall before the application can be submitted. The #1 audit finding, closed before it can happen.

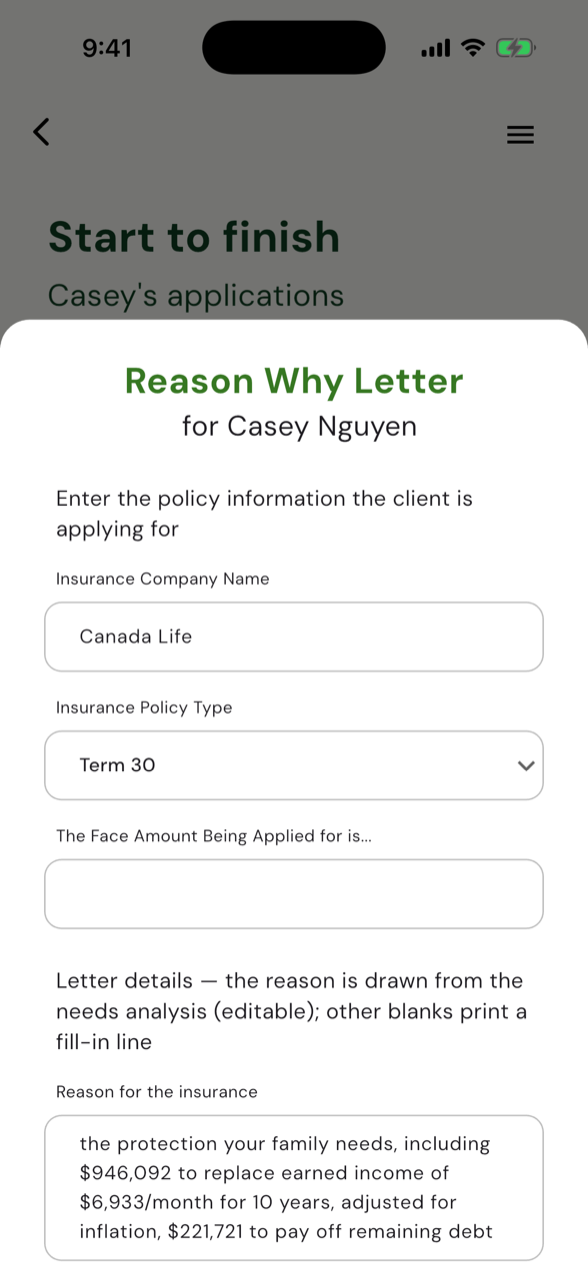

Explained, delivered, dated

New business gets a plain-language write-up of why you recommended what you did — delivered to the client with a dated proof of delivery. Delivered, not signed, exactly how the rule reads. No more digging for proof you sent it.

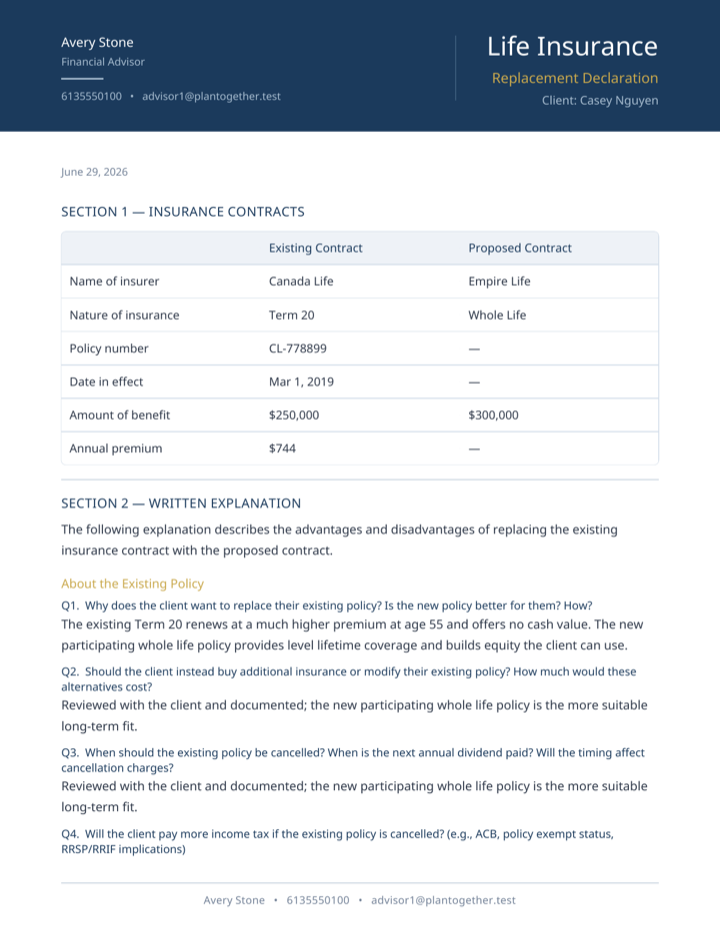

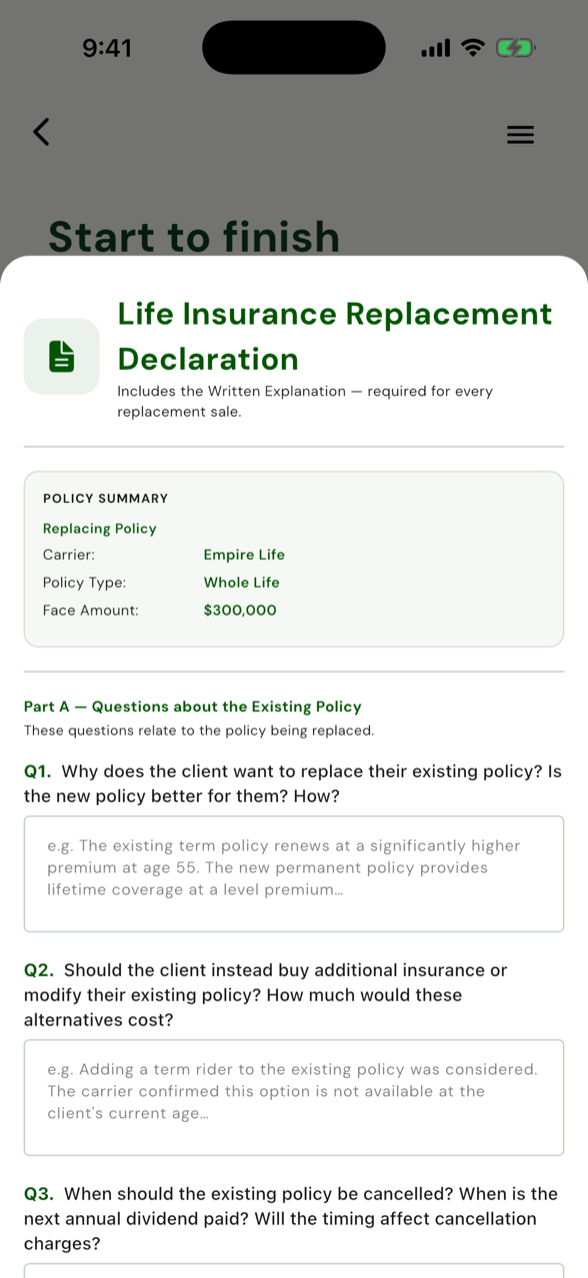

One toggle forks the whole path

Flag a replacement at sale-start and the sale reshapes: the Life Insurance Replacement Declaration snapshots the policy being replaced and gets signed before the application — standing in for the Reason-Why. Pick new business or replacement once, and you do the right document, never both.

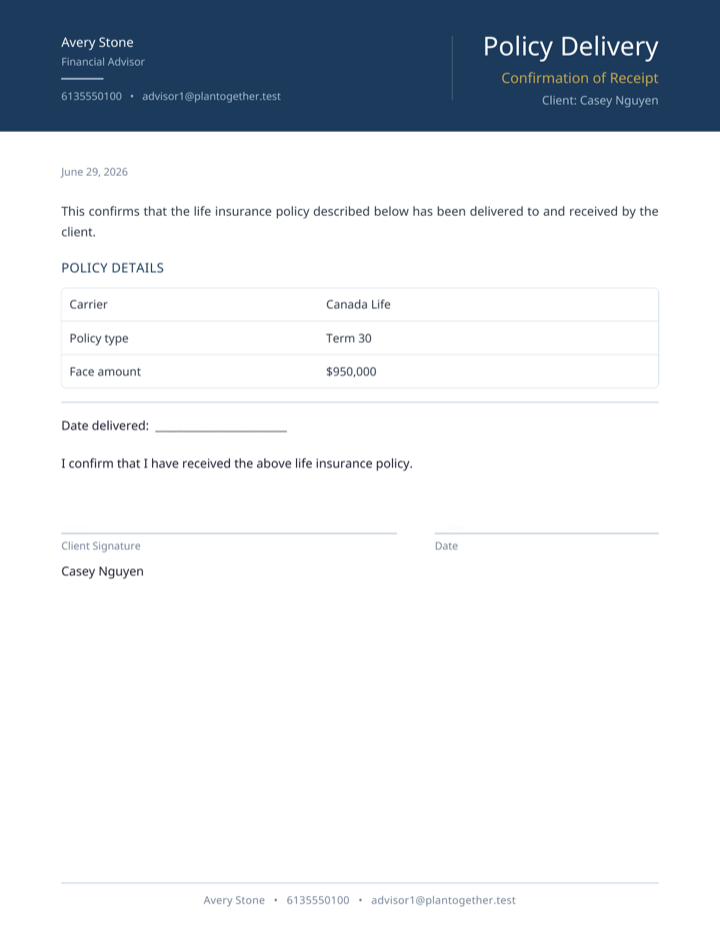

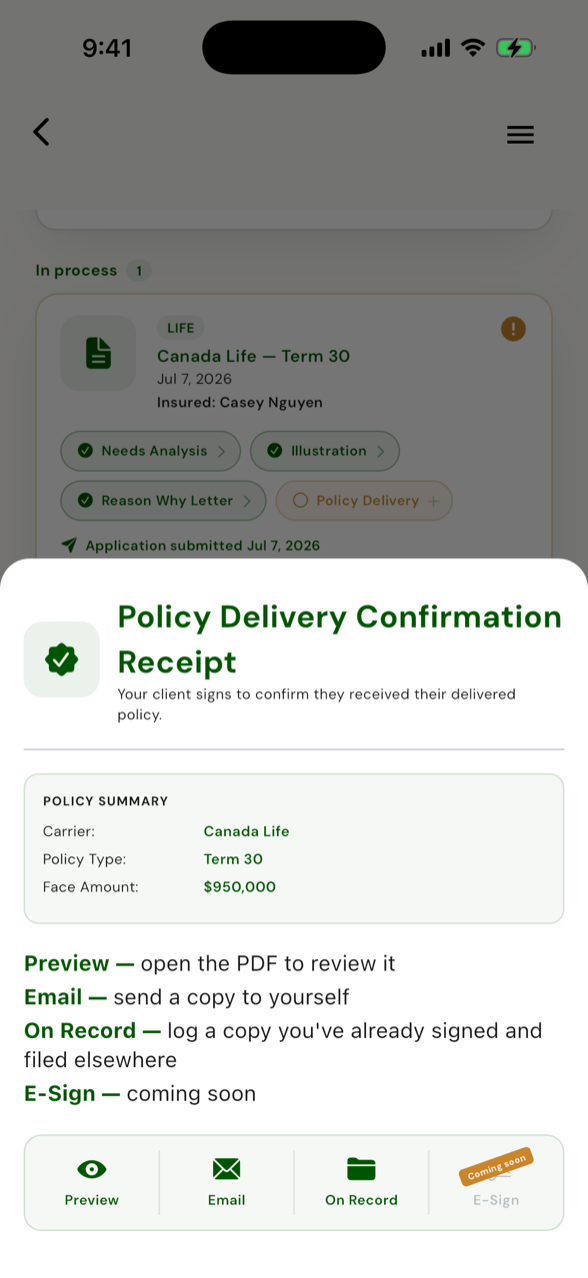

The client signs, the file seals

The client signs to confirm they received the policy. That signature seals the whole file: snapshots frozen, an in-force policy minted, nothing editable afterward. Tamper-evident, the way a finished file should be.

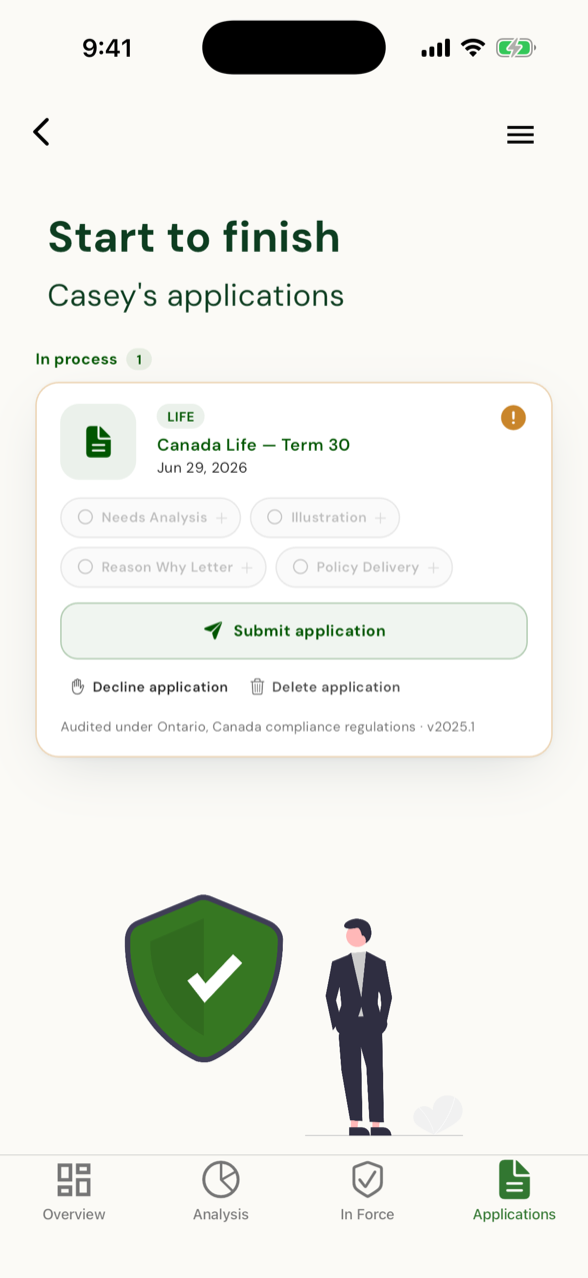

A locked sequence — and the file proves the order was followed.

A sale won't start until disclosure, privacy, and the fact find are signed. The needs analysis won't confirm while a shortfall sits un-acknowledged. Policy delivery stays locked, with a plain-English reason, until the reason-why is delivered. You can't skip a step or back-date the order — and the sequence itself is part of what gets audited. Hand-assembled forms fail audits because the dates land out of order. Here, they can't.

"The Reason-Why Letter must be generated and delivered before you can mark this policy delivered."

Every required document, signed and dated in the order the regulator audits.

That's the sale-level module. Client-Level Compliance — the always-on file checks — runs on every client whether they buy or not.

Two reasons. One app.

Give your clients an app they'll actually open — and let compliance keep itself, on every file and on every life sale. Spin up your shared workspace, invite a client, and watch one live file keep your plan current and your records audit-ready. Your first 5 clients are on us — no credit card.